中國的太空人,証明了中國有頂尖的科學家。中國的高鐵,証明了中國有領先世界的工程師。中國現在的亞投行,証明中國有金融高手了。

中國不缺人才,中國是一個有遠見、極爭氣的國家。中國在增長期,大家好好把握投資機會。

目前股市水平,A股太貴,暫不宜下手。

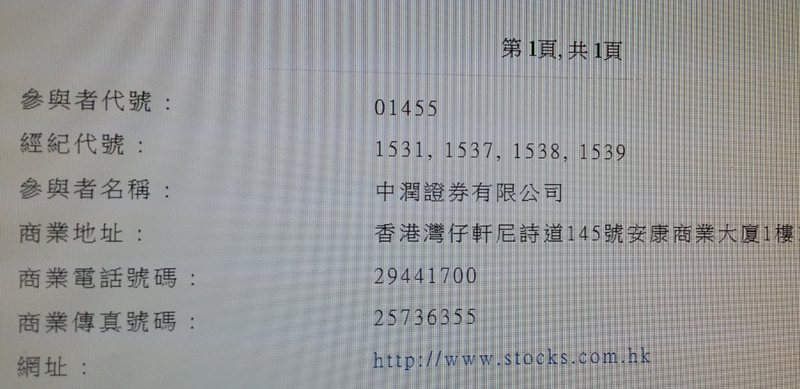

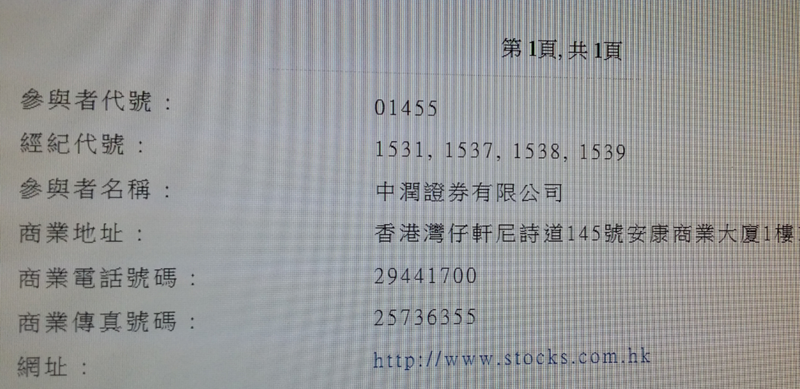

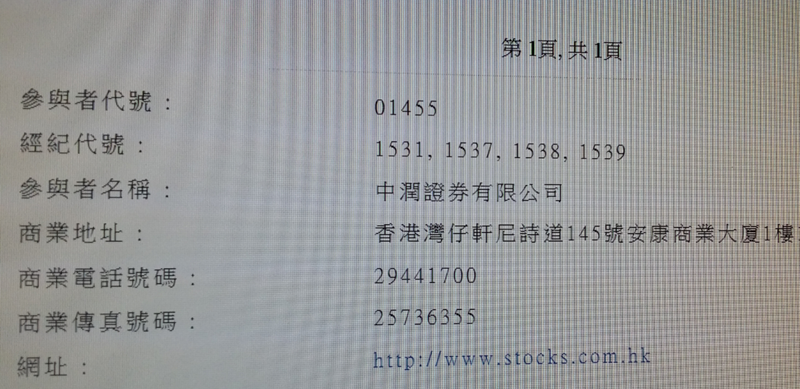

(本公司持有證券交易牌照、證券提供意見牌照、資產管理牌照。本公司是「滬港通」合資格参与者。)

當美國要增加軍費,就會說中國軍力擴張,大事宣揚中國威脅論。

當美國要為盟國撑腰,就說中國打不了現代戰爭,貶低中國軍隊。

中國不會介意有人說三道四,中國正在争取時間,專心一意壯大自己。

香港上市的軍工股值得投資。

中國的經濟特區非常成功,世界各國紛紛效法。緬甸、印度、非洲等國都在大量設特區。

世界各國都設立特區,難道政府發布一份特區公告,撥出一塊土地,提供賦稅減免,貧困地區就像變魔術,立即會繁榮昌盛? 有那麼容易嗎?

如果沒有可靠的政府,誰會去發展呢?那些國家學得來嗎?

中國現在又創新,搞自由貿易區了。

留意有關的股票。

人頭湧湧欣賞櫻花。

櫻花開花期是短暫的。香港股市今年上升期會是長期的。

本星期日, 3月15日下午6時,本公司主席蔡陳葆心女士接受無線電視翡翠台訪問,談及香港股市趣事......,避股災......,萬勿錯過,屆時請留意收看。

神州租車,我早前在上海租用此公司的汽車,取車的時候,車廂裏有果皮、廢紙。此公司管理需要改善。

最近此公司向我朋友買入一個買賣車網站域名,此公司將會發展買賣汽車業務。

日前我公司加薪又派發花紅。

回想過去年輕時,我曾經做過数份工,一晃就是十多年青春,無論過去的老闆是精明或刻薄,都有鋼鐵一般的鬥志,我很感激他們給我工作的機會,讓我獲得豐富的經歷。

多謝各位前任老闆,祝你們羊年大吉大利。

本公司持有證券交易牌照、證券提供意見牌照、資產管理牌照。本公司是「滬港通」合資格参与者。

減息啦,減息啦。

減息對什麼股票有利呢?

持有黄金是沒有利息的,所以息低,對黃金股有利。

減息,貸款者負擔減少,消費力可以提升,這類股可留意。

本公司持有證券交易牌照、證券提供意見牌照、資產管理牌照。本公司是「滬港通」合資格参与者。

香港議員爭吵的場面常在電視新聞出現。我發覺 : 有本事的人,没脾氣,沒本事的人,大脾氣。

(本公司持有证券交易牌照、证券提供意见牌照、资产管理牌照。本公司是“滬港通”合资格的参与者。)